Established in 1992, the Section 184 loan provided by HUD, the Department of Housing and Urban Development, has helped thousands of Native Americans get home loans both on and off reservations. For those who are looking for some quick tips about the HUD 184 loan, what is required for both home and borrower eligibility, and more, continue reading below.

Highlights

![]() No maximum income limits

No maximum income limits

![]() Low PMI monthly mortgage insurance

Low PMI monthly mortgage insurance

![]() Down payment requirement of 2.25%

Down payment requirement of 2.25%

![]() 1.5% one time, up-front guarantee fee that is financed into the loan

1.5% one time, up-front guarantee fee that is financed into the loan

![]() Needs to be an owner occupied primary residence only

Needs to be an owner occupied primary residence only

![]() NOT credit score driven, but but credit history will be reviewed

NOT credit score driven, but but credit history will be reviewed

![]() Homebuyer education is NOT required

Homebuyer education is NOT required

![]() Gifts of money funded by family or the tribe for assistance are allowed

Gifts of money funded by family or the tribe for assistance are allowed

Borrower Eligibility

![]() Must be in an approved Native American area (includes 39 states)

Must be in an approved Native American area (includes 39 states)

![]() Borrower can only have one HUD 184 loan at a time, once paid off, then borrower can apply for another one

Borrower can only have one HUD 184 loan at a time, once paid off, then borrower can apply for another one

![]() We need to have at least one enrolled member of a Federally Recognized Tribe, but they do not necessarily have to be related to, or married to the others on the loan.

We need to have at least one enrolled member of a Federally Recognized Tribe, but they do not necessarily have to be related to, or married to the others on the loan.

Property Requirements

Below are the property requirements for the HUD 184 loan that must be met, especially where the property is located:

![]() Needs to be a 1-4 single family residence

Needs to be a 1-4 single family residence

![]() Manufactured/Modular homes

Manufactured/Modular homes

![]() FHA approved condos

FHA approved condos

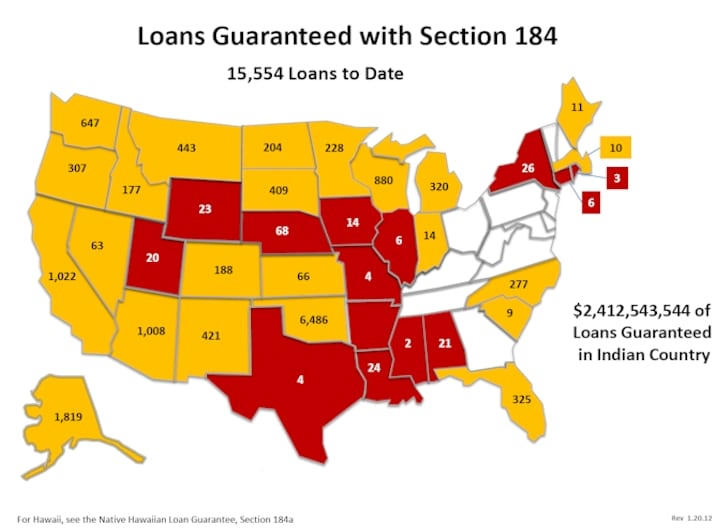

![]() Must be located on Section 184 eligible area (see the red and yellow map below) that has been approved

Must be located on Section 184 eligible area (see the red and yellow map below) that has been approved

184 Can be used in: Yellow – whole state, Red – certain counties, White – Ineligible

184 Terms and Limits

![]() The HUD 184 loan can be used for:

The HUD 184 loan can be used for:

![]() Purchase

Purchase

![]() Purchase and remodel/upgrade

Purchase and remodel/upgrade

![]() Rate and term refinance

Rate and term refinance

![]() Cash out refinance

Cash out refinance

![]() New Construction

New Construction

![]() Remodel/Upgrade

Remodel/Upgrade

![]() Debt Consolidation

Debt Consolidation

![]() 15 or 30 years fixed rate

15 or 30 years fixed rate

![]() Seller can contribute up to 6% seller concessions

Seller can contribute up to 6% seller concessions

![]() Max 41% DTI (debt-to-income) ratio

Max 41% DTI (debt-to-income) ratio

![]() Maximum loan limits will vary by county and state. Each has a different amount and here is a breakdown of each loan limit by state

Maximum loan limits will vary by county and state. Each has a different amount and here is a breakdown of each loan limit by state

Approved Lenders

There are approved lenders all across the country, including 1st Tribal. Eligible borrowers can apply, but must work with an approved 184 lender that have a deep understanding of the intricacies of the HUD 184 program. If you have any questions about what was covered in this post, or would like to know more information, feel free to contact us at 1st Tribal, call us at (866) 235-4033, or leave a comment below.