Hello readers and welcome to the “Do I Qualify for HUD Section 184 Loans 2” that is an extension of our earlier article Do I Qualify for HUD Section 184 Loans part 1! We here at 1st Tribal Lending are dedicated and here to help you figure out the sometimes difficult and frustrating process of taking out a home loan. So, below are some answers to some frequent questions that we’ve been asked, as well as some answer to questions that you might not even know to ask.

Does my credit have to be perfect to get the HUD 184?

Luckily, the HUD 184 program is not credit score driven in order to qualify for the loans and you don’t qualify based on your score alone. But, while we are reviewing your credit history there are certain things that are not good including open collection accounts, tax liens, judgments, and late payments that are 30 days or more. There is one exception, such as medical accounts if the IHS is responsible for it and will write a letter stating so.

If someone does not have any credit, we can use other and non-traditional methods of credit that do not show up on credit reports including: rent, power, cable, cell phone bills, water/utilities, car insurance, and more. These are all payments that can show your payment history. We are looking for payments on time for at least 12 months.

Do I have to be ‘low income’ to qualify?

No! You do not have to be considered ‘low income’ at all to qualify for the HUD 184 loans. You could technically earn any amount and qualify for the loans as long as you have at least 1 enrolled tribal member of a federally recognized* tribe on the loan in a tribe that has approved the use of the loan. You can use these loans to purchase, refinance, remodel/upgrade, or build your home.

*There are 5 state recognized tribes that have been grandfathered into the 184 program. It’s just a matter of looking it up to see if your tribe is a part of the program.

Do I have to get the loan where my tribe is?

We have received many questions about whether you can get the HUD 184 even if you live in a different town, or even state that the tribe you are enrolled in is located. As long as you are in an approved area for the loan and there is a person on the loan that is an enrolled member, you can potentially qualify for a HUD 184 loan, whether you are on or off rez. When tribal members are using the loan ON rez, that is the only time we have to make sure that the tribe has approved for the loan to be done, the tribe approves the loan to be done on their land. If you are using the loan OFF rez, then the tribe does not need to approve you to use it. An example: if a member of the Zuni tribe in NM wants to buy a home in Sacramento, CA, the tribe doesn’t need to approve them. But if the Zuni member wants to buy a home on Zuni tribal land, then the tribe must approve the 184 loan to be done on their lands. Here is a document of all tribes that have approved the HUD 184 loan program.

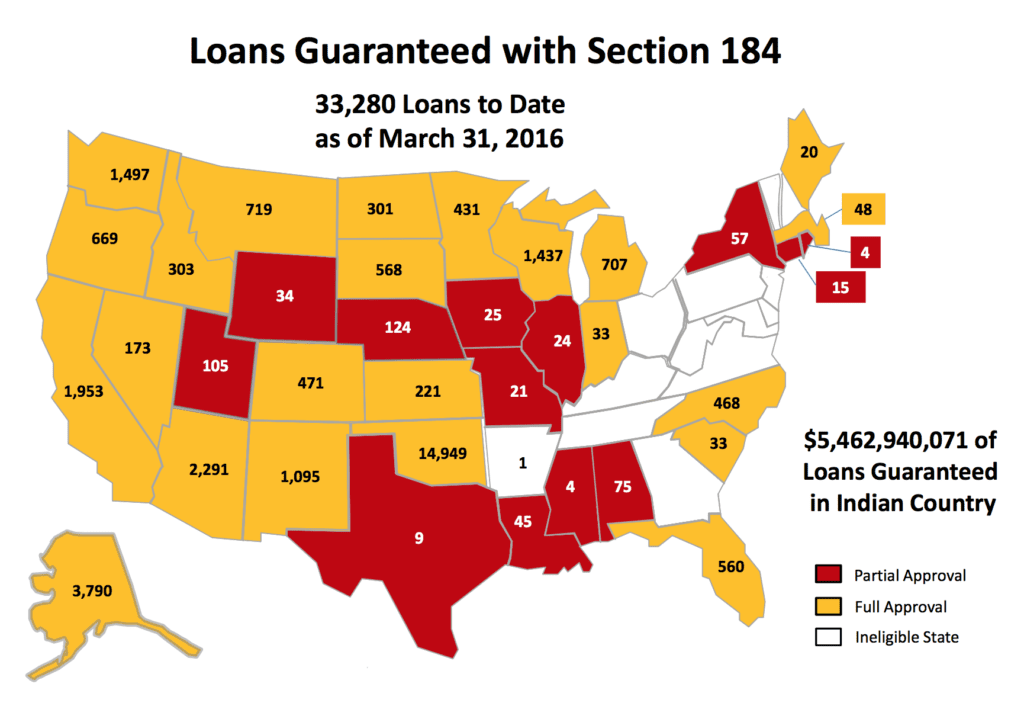

184 can be used in: Yellow – whole state, Red – certain counties, White – Ineligible

Does everyone on the loan need to be enrolled into a Native tribe?

No, not everyone on the loan has to be an enrolled member into a Native American tribe. In fact, the other persons on the loan can be non-native, as well as not even related or married to the enrolled member either! But, as long as there is at least 1 enrolled member of a federally recognized tribe who is a part of an approved tribe on the loan, then you will be able to qualify for the loan.

Some other helpful tips:

- You do not have to take a homebuyer educational class in order to get a HUD 184 home loan

- The HUD 184 loan does accept: down payment assistance either through family, friends, or grants from the tribe or state

- Your insurance, house payment, interest, and taxes (if required) are all in one payment for the HUD 184 loans

- There is NO payment penalty on the 184 Home loans

- We have to see at least one tribal enrollment card of someone on the loan in order to be accepted, we do not accept CDIB as proof of enrollment

- Self-employment income is accepted, we just need to see your taxes in order to know which loan amount you can qualify for

Have any more questions that we didn’t cover in this article? Please don’t hesitate to contact us here at 1st Tribal Lending either by telephone number: (866) 235-4033 or (510) 856-2184, email: webmaster@1tribal.com, or online at our website: https://www.1tribal.com/contactus/